Will the Australian property market crash?

With so much talk in the media about runaway inflation, surging interest rates and impending doom for the housing market, it's reasonable to be concerned about the future of Australian property.

Just how far is the downturn likely to go, though? Are we really in for a full-blown property meltdown, or will the market bounce back sooner than some are speculating?

After diving deeper into what industry experts are saying, things might not look so gloomy after all.

What are property price forecasts saying?

The big four banks speak loudest when it comes to forecasting what's going to happen in the market, and on average their outlook is certainly on the negative side.

Across 2022 and 2023 combined they expect the Australian median house price to fall by around -10 to -15 per cent as a result of rising interest rates and worsened affordability, among other things.

| Bank | 2022 national forecast | 2023 national forecast | Total change |

|---|---|---|---|

| Westpac | -2.0% | -8.0% | -10.0% |

| CBA | -6.0% | -8.0% | -14.0% |

| NAB | -3.7% | -14.0% | -17.7% |

| ANZ | -5.0% | -10.0% | -15.0% |

Sydney and Melbourne in particular are tipped to drop the furthest, somewhere around -20 per cent according to the big banks.

There are a few things worth pointing out here. Firstly, these potential declines are coming from national trough-to-peak growth of +28.6 per cent. It would take a monumental crash to wipe out those gains.

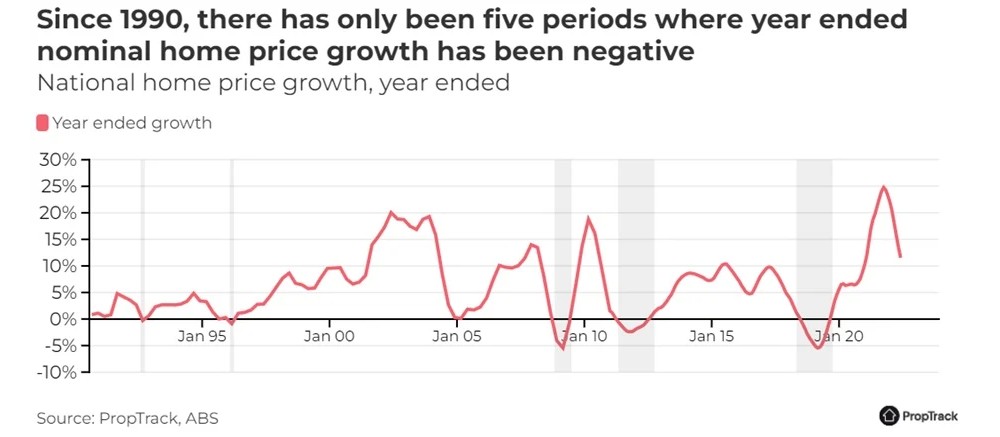

Secondly, such massive market corrections have never happened in Australia's history. PropTrack shows that, over the past 32 years, the five times a year has ended in negative growth has only resulted in relatively small corrections.

Finally, the banks' forecasts are notoriously conservative, and there's a strong chance that falls of -20 per cent or more won't eventuate.

Other economists like AMP Capital's Shane Oliver predict property prices to decline by around -10 to -15 per cent from their peak, and that includes the losses that most cities have already experienced.

What other opinions are out there?

While the banks' forecasts typically dominate media headlines, there is a wide range of views on the subject across the industry, many of which lean towards a more positive outlook.

Michael Yardney, one of the country's leading property experts and commentators, wrote in a Yahoo Finance piece that, while a correction was inevitable, "there is no property crash in sight."

"I agree, the RBA is going to have to ramp up interest rates and this will further stunt consumer confidence because, of course, that’s what it is intended to do," he said.

"And yes, property values will fall, but I can’t see falls of -15 or -20 per cent. The fact is property price falls of that magnitude have never happened before."

A growing number of economists and industry experts are predicting rate hikes will peak early in 2023 and may even be cut again later that year, which would help the market settle at its bottom sooner.

David Cassidy, Head of Investment Strategy at Wilson's Advisory, explained that "the RBA will be quite attuned to the impact of their rate rise cycle on house prices.

"The negative wealth effect from falling home prices will limit how much the RBA ends up raising rates. They will not want to crash house prices over the next 18 months (20 per cent or greater) and cause an economic recession."

What's in store for the Australian property market?

There are a variety of forces pushing from different directions that will all factor into the trajectory of the housing market.

Interest rates are one of the biggest, and it's all but a certainty that there will be further rate hikes over the next 6 months. The current cash rate is 1.85 per cent — the banks are forecasting it will hit anywhere between 2.60 per cent and 3.35 per cent.

| Month | CBA cash rate forecast | Westpac cash rate forecast | NAB cash rate forecast | ANZ cash rate forecast |

|---|---|---|---|---|

| Sep-22 | +0.5% | +0.5% | +0.5% | +0.5% |

| Oct-22 | +0.25% | +0.25% | +0.5% | |

| Nov-22 | +0.25% | +0.25% | +0.25% | +0.5% |

| Dec-22 | +0.25% | |||

| Feb-23 | +0.25% | |||

| Peak cash rate | 2.60% | 3.35% | 2.85% | 3.35% |

Whatever the outcome, that's going to continue to put downward pressure on property prices.

Affordability also remains a key issue, particularly in Australia's most expensive markets. Now, with buyers' borrowing power taking a hit, the problem is exacerbated.

On the other hand, the economy is strong. Unemployment is at record low levels, household savings remain high nationwide, and inflation may be tamed sooner than first expected.

Immigration is set to ramp up considerably after two dormant years, meaning demand for housing can only increase, and with fewer new construction projects lined up, there won't be the same degree of increase to supply.

With so many unknowns factoring into the equation, it's difficult to say just how things will turn out, but the worst-case scenario of a market crash is looking increasingly unlikely.

The market may find its floor once interest rate hikes end, and once that bottom is reached, the only way is up.