Revised 2026 outlook: property prices tipped to slow, but not everywhere

Just a few months ago, the 2026 property outlook looked reasonably settled as inflation was cooling and further interest rate cuts were on the horizon.

Then the conflict in the Middle East changed everything, spiking oil and energy prices in a matter of weeks, forcing the Reserve Bank to reverse course with three consecutive rate hikes — right before the federal budget introduced the biggest changes to property taxation in over a quarter of a century.

Find out what these sudden shifts mean for Australian property and why there's still reason for confidence in the market.

Get a free property value estimate

Find out how much your property is worth in today’s market.

The forecasts have changed — and the picture is still evolving

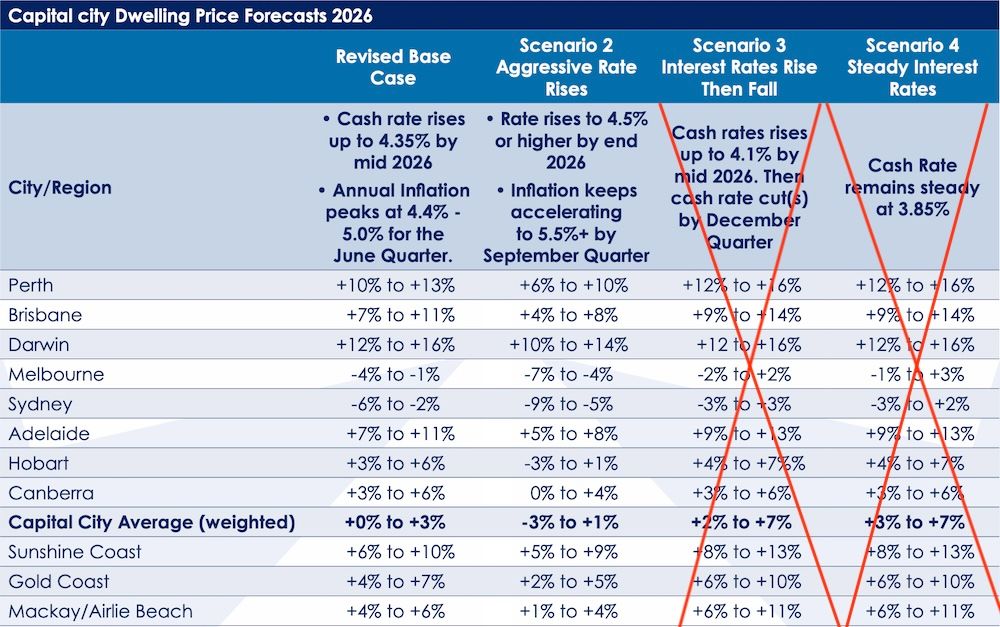

Recently, SQM Research took the unusual step of revising its annual Boom and Bust Report forecasts mid-cycle in response to the sudden market shakeup.

SQM's Louis Christopher proposed a new set of possible scenarios for the year ahead, with his base case assuming the cash rate peaking at 4.35 per cent — a level now reached following the latest hike.

Under that scenario, Mr Christopher now forecasts national capital city dwelling prices to grow somewhere between 0 and +3 per cent for the full year — down from the +6 to +10 per cent forecast published in November.

With the cash rate now at the base case peak, he is expecting Sydney housing prices to fall towards -6 per cent and Melbourne towards -4 per cent, while other cities are expected to slow but remain in positive territory for the year.

Writing in the wake of the RBA's May decision, Mr Christopher noted that the probability of a more severe Scenario 2, which would be triggered by even one further rate rise, has increased. That scenario would mean deeper falls in Sydney and Melbourne and a larger slowdown elsewhere.

The big four banks are now split on what comes next. ANZ and CBA consider May's hike to be the last of the cycle and are not forecasting further increases.

NAB, meanwhile, expects one further rate lift in August, while Westpac is the hawkish outlier, forecasting two more hikes in August and September. That would push the cash rate to 4.85 per cent, a level not seen since 2008.

The path forward for interest rates and property price growth is closely tied to the inflation outlook which, given the level of volatility we're seeing around the Middle East, is something even the most credible forecasters can't meaningfully pin down.

However, independent property economist Cameron Kusher added some important context about where the problem actually started.

"It would be easy to point the finger here at the Middle East situation, and it is going to exacerbate these issues the longer it continues," he said. "But the reality is that inflation was too high before this situation arose."

Some markets are feeling it more than others

The rate environment doesn't hit every market the same way, and SQM's revised forecasts reflect that clearly.

Sydney and Melbourne are bearing the brunt. Both cities have historically moved more sharply in response to rate changes, and this cycle is no different. SQM's base case puts Sydney at between -2 and -6 per cent for the year and Melbourne at -1 to -4 per cent.

Perth, Brisbane, Darwin, and Adelaide are a different story. These markets benefit directly from the same commodity price surge that is driving inflation nationally, with higher oil, gas, gold, and coal prices flowing through into local wages, royalties, and employment — providing a real economic buffer against the rate headwind.

There's also a demand dynamic worth keeping in mind across all markets. As borrowing capacity tightens, buyer competition tends to concentrate at the more affordable end of the market, which can be good news for sellers in that segment.

With rental vacancy rates sitting at just 1.1 per cent nationally — one of the tightest readings on record — a growing number of tenants are also feeling the pressure to buy rather than keep competing for a shrinking pool of rentals, adding further weight to demand at the entry level.

What the federal budget means for the property market

The 2026 federal budget delivered the biggest change to property taxation in more than a quarter of a century, adding another layer to an already complex outlook.

From 1 July 2027, negative gearing on established residential properties will be restricted — rental losses can no longer be offset against other income like wages, though they can be carried forward against future rental income or capital gains.

Negative gearing on newly built properties remains fully available. The existing 50 per cent capital gains tax discount will also be replaced with cost-base indexation and a new 30 per cent minimum tax on real gains from that date.

Importantly, any property already owned or under contract at 7:30 pm AEST on 12 May 2026 is fully grandfathered under the old rules. And for owner-occupiers selling their primary residence, the main residence CGT exemption is completely untouched — these changes target investment properties, not family homes.

CBA Senior Economist Trent Saunders modelled the combined impact and found the effect on prices, while real, is modest.

"House prices are expected to be just under 3% lower than they otherwise would have been," he said, noting the effect plays out gradually over several years with a peak drag of around 1 percentage point on annual price growth.

As Westpac Economics noted in its budget analysis, "in the short term, the interest rate environment will be a more consequential influence" on the housing market than these tax reforms.

The budget does include $2 billion for housing infrastructure and $500 million to streamline planning approvals — both aimed at addressing the structural undersupply that has underpinned property values over the long term.

For a full breakdown of what the budget changes mean, read our complete guide to the 2026 budget and property.

The longer-term picture for sellers remains intact

For all the uncertainty in the current headlines, there's data that puts things in perspective.

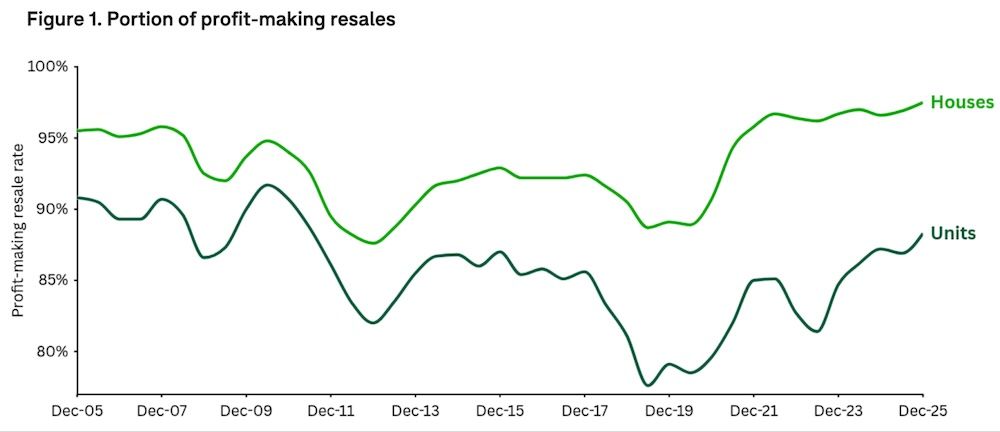

Domain's 2026 Profit and Loss Report found that 97.5 per cent of house sellers across Australia made a profit in the second half of last year — a record-high ratio.

The median house resale profit nationally was $440,000, with Sydney at $750,000 and both Brisbane and Perth recording record medians of $580,000 and $528,000 respectively.

These profits weren't generated by people who timed the market perfectly. As the Domain report notes, the typical Australian property owner holds for around nine years before selling — long enough to ride through multiple rate cycles, including ones that looked a lot like this one.

Mr Kusher's longer-term read is worth keeping in mind, too. "While the impact of higher inflation and higher interest rates for longer is likely to be lower housing prices...longer-term these conditions are likely to sow the seeds of the next surge in housing prices," he said.

The current environment is genuinely challenging, particularly in Sydney and Melbourne where buyers are more cautious and the market has less room for overpricing.

For most sellers, though, the years already spent in the market have done a lot of the hard work. A realistic price and a strong local agent matter more right now — not less.