What the March interest rate hike means for Australian sellers

Interest rates have risen for a second time in as many months as the fight against inflation continues, creating further uncertainty in Australia's housing markets.

It's a move that presents challenges to current and would-be homeowners around the country, but the immediate impact is often more complex than the headlines suggest.

We'll cut through the noise to run through why rates are rising, what it means in the short term, and how our property markets could be affected throughout 2026.

Get a free property value estimate

Find out how much your property is worth in today’s market.

Why did the RBA hike rates again?

Towards the end of 2025, there was broad optimism that the new year would bring further rate cuts and a neatly contained inflation rate.

However, conditions shifted quickly in 2026. By February, the Reserve Bank of Australia (RBA) was forced to change its tune and hike the cash rate by 0.25 per cent after inflation began to climb above the central bank's target range again.

This week, the RBA announced another hike in response to a muddier inflation outlook. There are a few key drivers to keep an eye on:

- Global energy shocks: The escalating conflict in the Middle East has sent shockwaves through global energy markets. With oil prices hitting high levels and coal prices on a tear, these global issues are flowing directly into the price of petrol and electricity here in Australia.

- Persistent inflation at home: It’s not just the price of fuel that’s the problem; services inflation (the cost of things like insurance, eating out, and professional services) is proving much harder to bring down than the RBA anticipated.

- A very tight job market: Even with higher rates, almost everyone who wants a job has one. Low unemployment is generally a good thing, but it also means people are still out there spending, which keeps the economy running a bit too hot for the RBA's liking.

While the RBA board itself admitted the call to hike in March was a marginal one, it was made in an effort to stamp out any chance of inflation spiralling out of control as it did in 2022, even if it means short-term pain for mortgage holders.

How will Australian property markets respond to the hike?

While a rate hike is never the news buyers or sellers want to hear, the immediate impact on the market is often more complex than a doom-and-gloom headline might suggest.

In the short term, the most direct effect is on borrowing power. Independent property expert Cameron Kusher noted that this latest move will reduce mortgage borrowing capacity by around 2.5 per cent, but it can also trigger a brief burst of activity.

"For those looking to purchase, the rate hike may also create some urgency, especially for those buyers with pre-approval who want to buy before their approval expires," Mr Kusher said.

For sellers, this means there is a window of highly motivated buyers currently in the market who are eager to ink a deal before their bank reassesses their paperwork and potentially offers them a smaller loan.

Looking more broadly, SQM Research recently revised its Boom and Bust report outlook, suggesting that we could see a widening gap between the major capitals.

Sydney and Melbourne have traditionally been more sensitive to rate moves. SQM's Louis Christopher pointed out that Sydney’s auction clearance rates have recently hovered around 46 per cent.

Historically, when clearances sit below the 50 per cent mark at the start of the year, it suggests that buyers are becoming more cautious and price growth may start to level off, as recent data already shows.

Perth, Brisbane and Adelaide, meanwhile, have continued to show remarkable resilience. Christopher's latest report suggests that these markets are currently benefiting from high commodity prices and an income injection into their local economies. As a result, they're better positioned to absorb a rate hike without losing momentum.

On a national level, the latest Oliver Hume Land Index & Residential Outlook report posed the argument that the drive for security through housing will continue to keep the property market moving forward.

Oliver Hume's CEO, Julian Coppini, said "Australians have an insatiable appetite for home ownership, and that aspiration has not changed, regardless of the rate cycle or the headlines of the day."

Will any further rate hikes mean lower property prices?

There are two big questions being asked by many Australians this week: are we going to see more rate hikes, and will property prices fall as a result?

In terms of the RBA's next decision, the Big Four banks are predicting another hike to 4.35 per cent in May, bringing the cash rate back to its previous peak level before holding steady for the remainder of 2026.

But with so much uncertainty about how the conflict in the Middle East will play out, no next steps can be confidently ruled in or out at this stage.

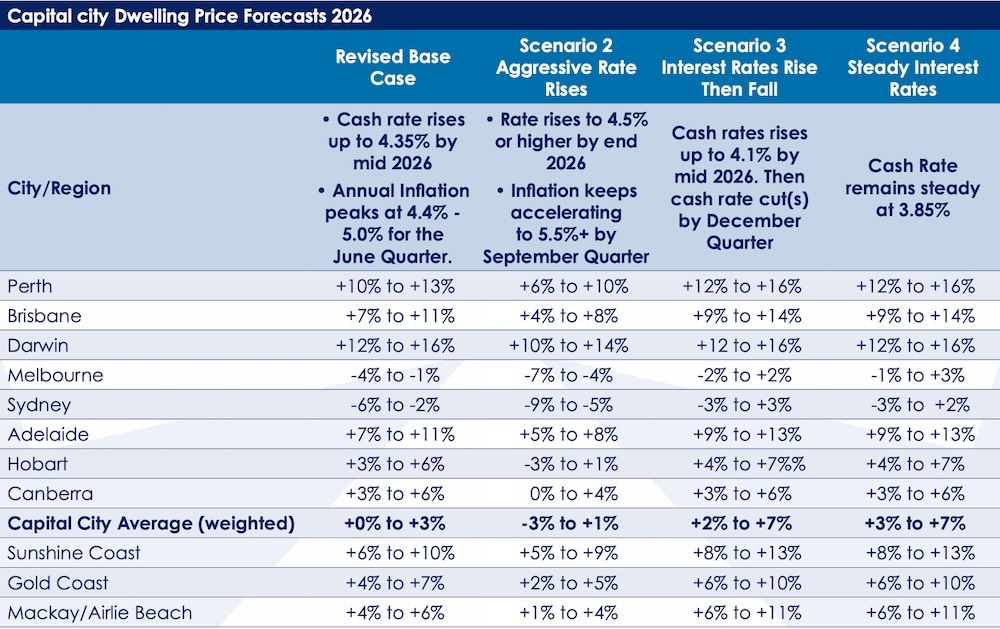

Given the complexity of the situation, SQM Research has offered up four new scenarios for 2026 and how each could affect property price growth around Australia.

Their base case scenario continues to project strong gains for the mid-sized capitals and Darwin, with Hobart and Canberra also tipped for reasonable growth.

Sydney and Melbourne, however, may see a dip. Christopher noted that both markets have "historically been more susceptible to adverse interest rate changes than the capital city average," and growth in each city has already flattened out so far in 2026.

Ultimately, while the headlines focus on macroeconomic shifts, the property market is still widely driven by life stages. People still need to downsize, families still need to upsize, and buyers are still looking for quality homes regardless of a change in interest rates.

The key for sellers in 2026 isn't to panic, but to be prepared. By focusing on a realistic pricing strategy and the long-term capital growth of your property, this part of the cycle can still be navigated with confidence. The market may end up moving at a different speed than it was last year, but it is certainly still moving.